From carbon cost to profit driver: How CFOs can turn climate risk into strategic value

The article explains how CFOs can turn climate risk into a strategic, financially driven value opportunity by integrating robust carbon accounting into core financial planning, risk management, and capital allocation.

Sign up to get full access

Link

Introduction

Climate change is already showing up in financial results, from supply chain interruptions and facility downtime to higher insurance premiums and energy costs. Meanwhile, expectations from customers, lenders, and investors are shifting toward clearer disclosure of climate risks and credible decarbonization plans. This creates a growing tension for leadership teams that need to balance short term performance, long term resilience, and an increasingly complex sustainability agenda.

At the same time, the regulatory environment is confusing.The European Union has delayed sector specific European Sustainability Reporting Standards and rules for non EU companies to 2026 to give firms more time to implement the first CSRD standards, and is considering higher thresholds and reduced reporting burdens for some companies as part of a simplification agenda. Similar uncertainty surrounds climate reporting in other jurisdictions. It can be tempting for management teams to pause and wait.

The climate itself is not waiting. Physical risks are intensifying, carbon prices are expanding through mechanisms such as EU ETS and the upcoming ETS2, and customers and investors are tightening expectations. In this environment, climate risk and decarbonization cannot quietly fall off the corporate radar. Someone has to make sure they are quantified, managed, and, ideally, turned into sources of strategic advantage.

That someone is the CFO—the person who owns financial risk, capital allocation, planning, and performance management. Climate risk now cuts across all of these domains. To manage these challenges, CFOs need robust carbon metrics that are as structured and reliable as financial data, alongside separate assessments of broader climate risks such as physical impacts and supply chain exposure. Carbon accounting does not cover every aspect of climate risk, but it is a critical foundation for understanding emissions, carbon price exposure, and progress against targets.

The CFO mandate in a changing climate

For most companies, climate risk is now financial risk:

- Physical risk affects asset values, downtime, insurance costs, and supply chain continuity.

- Transition risk affects energy and fuel costs, logistics rates, carbon taxes, and customer demand.

- Liability and reputational risk influence access to capital, funding costs, and valuation. Strong ESG ratings can improve financing conditions, and accurate CO₂ accounting is a key ingredient for performing well on the climate dimension of those ratings.

Deloitte and others argue that climate related risk should be integrated into mainstream enterprise risk management, scenario analysis, and planning, rather than treated as a separate ESG silo. This integration needs clear sponsorship from the CFO and finance, in close partnership with sustainability, risk, and operations.

To deliver, the CFO and their team need finance grade carbon data that:

- maps emissions to business units, cost centers, products, and customers

- flows from the same source systems that drive financial reporting

- is checked through validation and internal controls that resemble audit processes

- feeds climate strategy, transition planning, and capital allocation

This is the role of modern carbon accounting software and of a finance oriented climate strategy. It creates a single emissions ledger that sits alongside the general ledger and enables the CFO to treat carbon in a similar way to money.

Short term (0 to 12 months)

Keeping climate on the reporting and budgeting agenda

In CFO language, the short term corresponds to the current and next reporting cycles: year end, audited financials, risk disclosures, and the upcoming budget.

Priorities in the short term

- Establish a finance grade carbon baseline

- Map emissions sources to financial structures such as cost centers, business units, and product lines.

- Deploy carbon accounting software that ingests data directly from ERP, procurement, transport management systems, and energy providers, instead of relying on disconnected spreadsheets.

- Introduce monthly or quarterly carbon closes that run alongside financial closes.

- Map emissions sources to financial structures such as cost centers, business units, and product lines.

- Connect climate impacts to financial statements

- Review recent weather and climate related incidents, such as supply chain delays or facility interruptions, and estimate their financial impact where possible. In parallel, identify long lived, high emission assets, for example machinery that can run only on fossil fuels for 15 to 20 years, which may lock in future emissions and costs.

- Reflect climate sensitive assets and exposures in impairment tests, risk reports, and management commentary.

- Review recent weather and climate related incidents, such as supply chain delays or facility interruptions, and estimate their financial impact where possible. In parallel, identify long lived, high emission assets, for example machinery that can run only on fossil fuels for 15 to 20 years, which may lock in future emissions and costs.

- Prepare for near term carbon cost pass through

- EU ETS already covers power and heavy industry and now shipping. ETS2 for road transport and buildings will start in 2027. The European Commission expects ETS and ETS2 carbon prices to move toward roughly 100 to 122 euros per ton of CO2 by 2030, which could raise fuel prices for road transport and buildings significantly. Introducing an internal carbon price in project and planning models helps companies prepare for this reality before it fully shows up in invoices.

- These cost increases are likely to appear as fuel and freight surcharges, higher energy bills, and embedded costs in purchased materials and services.

- EU ETS already covers power and heavy industry and now shipping. ETS2 for road transport and buildings will start in 2027. The European Commission expects ETS and ETS2 carbon prices to move toward roughly 100 to 122 euros per ton of CO2 by 2030, which could raise fuel prices for road transport and buildings significantly. Introducing an internal carbon price in project and planning models helps companies prepare for this reality before it fully shows up in invoices.

Example: logistics heavy retailer

A European omnichannel retailer sees its ocean freight invoices start to include new carbon surcharges linked to shipping emissions. The finance and logistics teams use integrated carbon accounting software to break down emissions and carbon related costs by route, carrier, and product category.

The CFO works with procurement and operations to tackle the most carbon intensive transport first, for example by shifting suitable shipments from air to sea, consolidating loads, and, where air freight is unavoidable, using book and claim or lower emission options even if they come with a cost premium. The carbon accounting system provides the data to compare cost and emissions for these choices.

Example: manufacturer with a flood exposed plant

A component manufacturer operates a critical plant in a river valley that has experienced two significant floods within a decade, with rising insurance premiums. The CFO uses a combination of climate data and past loss events to estimate the expected value of flood related losses over the next five years, then compares this with the capex required for flood defenses and resilience upgrades.

The climate adaptation measures are approved as an investment with a clear payback period, and their rationale is documented in the risk register and internal investment cases. While this is primarily about physical climate risk rather than emissions accounting, it follows the same logic: turning climate related exposures into quantified, managed financial decisions..

Medium term (2 to 5 years)

Embedding climate and carbon into transition planning and capital allocation

The medium term is the horizon of strategic plans, rolling forecasts, and transition plans under frameworks such as CSRD, TCFD or ISSB, CDP, and SBTi.

Why this horizon matters

- Carbon pricing tightens through EU ETS and ETS2, with higher prices and broader coverage that raise energy and fuel costs into the 2030s.

- CBAM progressively prices the embedded carbon in imports of steel, cement, aluminum, fertilizers, electricity, and more, influencing procurement economics.

- Large customers increasingly demand supplier emissions data and credible reduction plans as a condition of doing business.

BCG estimates that failing to decarbonize supply chains could lead to very significant additional annual costs globally by 2030, while many supply chain decarbonization measures can deliver returns of three to six times their cost. Examples include co-investing in energy efficiency upgrades at key suppliers, optimizing transport modes for high volume lanes for instance shifting from air to sea or rail where lead times allow and reducing material use in packaging. These kinds of interventions can cut emissions and lower unit costs at the same time, creating mutual benefits for both buyer and supplier.

CFO levers in the medium term

- Internal carbon pricing and adjusted hurdle rates

The CFO can introduce an internal carbon price that mirrors expected EU ETS and ETS2 levels and sector benchmarks. Projected net present values, which represent the present value of expected future cash flows, and hurdle rates, representing the minimum acceptable return, can include the cost of emissions and avoided emissions. - Transition planning as capital planning

Transition plans should not be treated as compliance documents, but as forward looking capital allocation roadmaps. Carbon accounting software can support this by providing marginal abatement cost curves, reduction scenarios, and clear views of how much emissions and cost each measure can remove. - Supplier engagement and contract strategyMany medium term emissions and cost reductions sit in the supply chain. The CFO can work with procurement to embed carbon considerations into supplier selection, pricing models, and contract terms for example by linking preferred terms or co-investment to clear reduction targets and by using carbon data to identify joint efficiency gains that benefit both buyer and supplier.

Example: logistics company preparing for ETS2

A pan European logistics provider expects effective carbon costs on fuel under ETS2 to move toward 90 to 100 euros per ton of CO2 by 2030, based on European impact assessments. The CFO sets an internal carbon price of 100 euros per ton in internal investment models from 2026 onward.

Using carbon accounting software that is integrated with fleet, route, and depot data, the company builds a transition plan that phases in electric and biofuel trucks on high density routes, invests in energy efficient depots with on site solar, and designs low carbon logistics products for key customers at a premium.

As actual ETS and fuel prices rise, the company absorbs costs more easily than competitors, maintains margins, and grows its share in low carbon freight offerings.

Example: industrial manufacturer and supplier decarbonization

An industrial equipment manufacturer discovers that about 70% of its supply chain emissions come from fifteen suppliers of metals and castings. Scenario analysis shows that simply passing through expected carbon prices to these suppliers by 2030 would increase product input costs by 4 - 6%.

The CFO creates a supplier decarbonization program that offers co financing, longer contracts, or better terms in exchange for concrete emissions reductions, tracked in the same platform used for procurement and carbon data. The company reduces Scope 3 emissions while containing the cost of goods sold and strengthening critical supplier relationships.

Long term (5 to 15 plus years)

Resilience, strategic optionality, and valuation

The long term is the horizon of asset lives, product platform decisions, and equity valuation. Plants, logistics hubs, and data centers often maintain viability for decades, and investors increasingly scrutinize exposure to long term physical climate risk and deep transition uncertainty.

McKinsey research indicates that by 2050 some regions could face several times today’s risk of coastal flooding, extreme heat, or severe storms, which could render assets in these areas uninsurable or uneconomic without significant adaptation. For CFOs, these are questions about capital deployment, stranded asset risk, and long term return on invested capital.

Long term CFO priorities

- Location and asset strategy

- Integrate physical climate risk maps into site selection, plant expansion, and M&A due diligence.

- Require climate adjusted cash flow scenarios as part of all major capex decisions.

- Integrate physical climate risk maps into site selection, plant expansion, and M&A due diligence.

- Capital structure and insurance

- Anticipate that insurance and reinsurance may become more expensive or restricted in high risk regions.

- Explore catastrophe bonds, resilience financing, and blended finance instruments to fund adaptation.

- Anticipate that insurance and reinsurance may become more expensive or restricted in high risk regions.

- Strategic options around business models

- Use carbon and climate scenario analysis to evaluate where to double down, divest, or fundamentally transform business lines, based on likely carbon price paths, customer demand shifts, and physical risk.

- Use carbon and climate scenario analysis to evaluate where to double down, divest, or fundamentally transform business lines, based on likely carbon price paths, customer demand shifts, and physical risk.

Example: chemicals company choosing a new plant location

A chemicals company is choosing between building a new plant in a coastal industrial cluster with excellent port access, or an inland site that is somewhat more expensive in terms of land and logistics.

By combining climate risk maps, carbon scenarios, and financial modeling in its planning tools, the finance team finds that the coastal site faces a two to threefold increase in flood risk by mid century, which could reduce NPV by 15 - 20% once downtime, repairs, and higher insurance costs are included. The inland site has slightly higher transport emissions today, but is better positioned for low carbon rail and pipeline options under higher carbon prices on fuel.

The CFO recommends the inland site. The decision avoids the risk of a future stranded asset and strengthens the long term transition story the company can tell investors.

What carbon accounting integration looks like in practice

To keep climate risk and decarbonization embedded in financial decision making across all these time horizons, CFOs, sustainability leaders, and compliance officers need a shared data and control backbone.

Modern carbon accounting software can mirror the architecture of financial systems.

- Structured emissions ledger

Every emissions record has a source, timestamp, and allocation logic, so data can be aggregated and drilled down by site, business unit, process, product, and customer, in the same way as financial data. - Validation and controls

Data completeness checks, plausibility rules, outlier detection, and benchmark comparisons give a quantified sense of data quality. Audit logs record how data was transformed and calculated, which supports CSRD and assurance needs. - Integration with ERP, BI, and planning tools

Inbound connections pull activity, spend, and emissions data from ERP, accounting, procurement, transport management, and energy systems. Outbound connections feed validated carbon data into ESG reporting (CSRD, CDP, SBTi, Ecovadis), BI dashboards, and planning models. - Insights and decarbonization intelligence

Scenario planning, internal carbon pricing, ROI and payback analysis, and carbon specific performance indicators help finance and sustainability teams jointly answer where to invest, what to change, and what value that will create.

This creates a practical collaboration model:

- Sustainability brings emissions expertise and reduction levers.

- Finance brings investment criteria, portfolio management, and performance steering.

- Compliance and internal audit ensure that processes and data stand up to regulatory and assurance scrutiny.

Working from a single, validated carbon dataset, these teams can prevent climate risk and decarbonization from slipping off the agenda when other pressures rise, and instead use them to sharpen business performance.

How Cozero supports CFOs in this role

Cozero is built on the idea that emissions data should be as central and reliable as financial data, so that enterprises can manage carbon with the same discipline and intelligence they apply to money.

The platform focuses on the capabilities that matter most to CFOs:

- Data ingestion and connectivity

Cozero connects to ERP, procurement, logistics, and energy systems to automate the intake of activity, spend, and emissions data. This significantly reduces the time from first connection to decision ready information, so climate considerations can be part of the same reporting and planning cycles that finance already runs. - Data validation and controls

Cozero provides a finance grade validation layer with completeness checks, plausibility rules, benchmarking, and audit logs. This helps companies generate CSRD, CBAM, CDP, and SBTi disclosures from carbon data that is traceable, consistent, and ready for assurance. - Insights and decarbonization intelligence

Cozero links emissions to cost, ROI, and carbon prices, enabling marginal abatement cost curves, internal carbon pricing, and climate informed capital allocation. CFOs and sustainability leaders can evaluate decarbonization measures, supplier programs, and asset decisions through a climate adjusted financial lens, across short, medium, and long term horizons.

In a world where regulation may slow or shift but climate impacts and carbon costs are clearly rising, this kind of integration is what keeps climate risk and decarbonization squarely on the CFO’s docket, not as a compliance obligation, but as a driver of resilience, competitiveness, and long term value creation.

Sources

- Council of the EU. (2024). Council and Parliament agree to delay sustainability reporting for certain sectors and third-country companies by two years. Retrieved from https://www.consilium.europa.eu/en/press/press-releases/2024/02/07/council-and-parliament-agree-to-delay-sustainability-reporting-for-certain-sectors-and-third-country-companies-by-two-years/

- European Commission. (2025). Trends in carbon intensity and the macroeconomic role of the EU Emissions Trading System. Retrieved from https://economy-finance.ec.europa.eu/trends-carbon-intensity-and-macroeconomic-role-eu-emissions-trading-system_en

- Boston Consulting Group. (2025). From liability to advantage: Decarbonizing the supply chain. Retrieved from https://www.bcg.com/publications/2025/liability-to-advantage-decarbonizing-supply-chain

- McKinsey & Company. (2020). Can coastal cities turn the tide on rising flood risk? Retrieved from https://www.mckinsey.com/~/media/mckinsey/business%20functions/sustainability/our%20insights/can%20coastal%20cities%20turn%20the%20tide%20on%20rising%20flood%20risk/mgi-can-coastal-cities-turn-the-tide-on-rising-flood-risk.pdf

- European Parliament. (2025). Sustainability reporting and due diligence: MEPs back simplification changes. Retrieved from https://www.europarl.europa.eu/news/en/press-room/20251106IPR31296/sustainability-reporting-and-due-diligence-meps-back-simplification-changes

Related articles

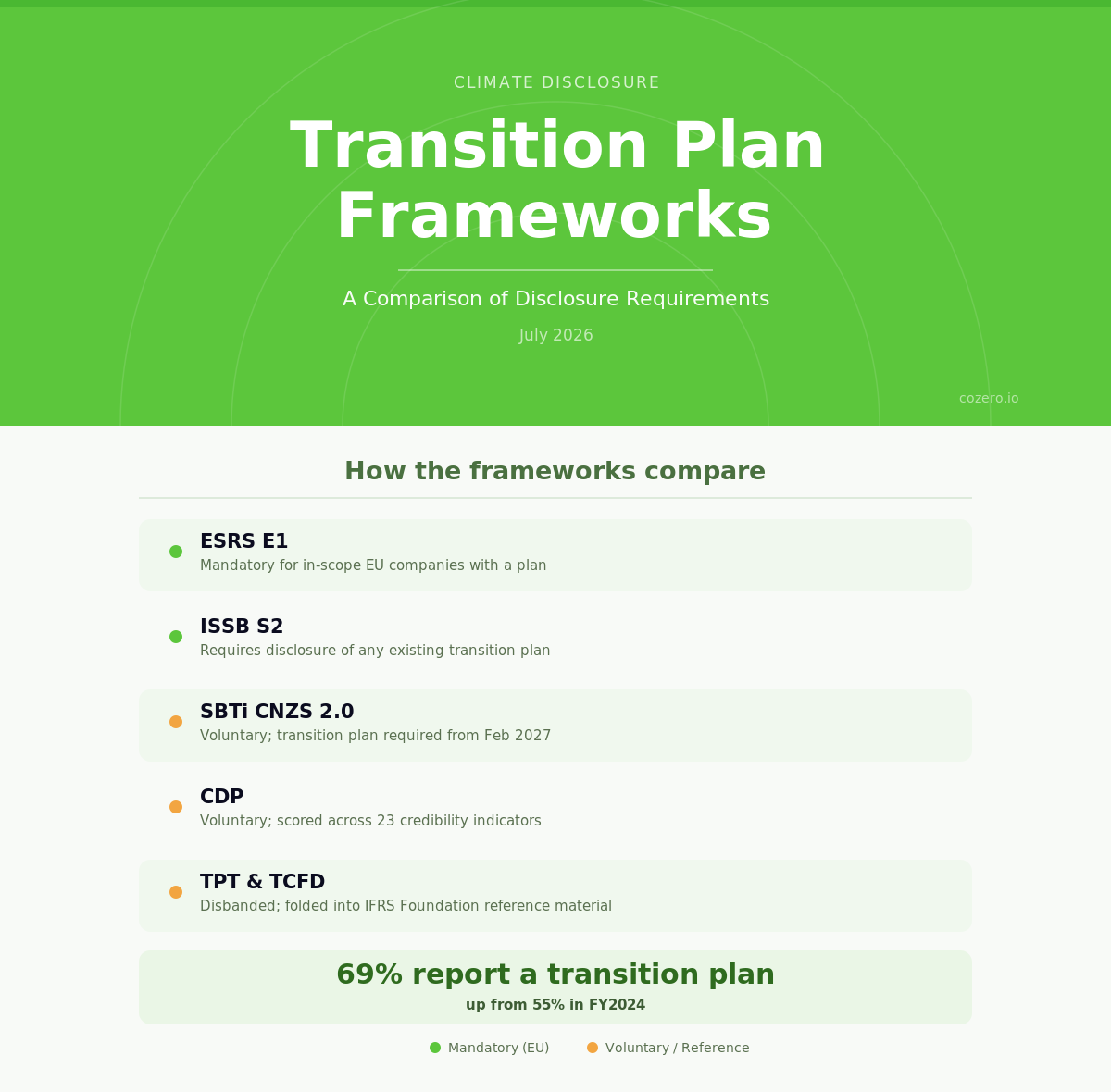

Climate Transition Planning Frameworks: A Comparison of Disclosure Requirements