CSRD in Flux: What the 2025 Trilogues Could Mean for Logistics, Manufacturing, and Other Scope-3-Intensive Industries

In this article, Cozero's Climate Expert Esther Snijder explains how the EU’s “Stop-the-Clock” directive delays CSRD reporting and why this pause is a strategic opportunity for companies to strengthen emissions data, supplier engagement, and governance to stay ahead when reporting resumes.

Sign up to get full access

Link

Introduction: A regulatory cliffhanger for Europe’s value chains

If European sustainability policy were a Netflix series, the current moment in Corporate Sustainability Reporting Directive (CSRD) implementation would be the mid-season twist. Suddenly the plot has deepened, deadlines have shifted, and the next episode will not start until the trilogue resumes. In October 2025, the European Parliament voted to reject a mandate on the simplification package, postponing negotiations until its next plenary vote in November, which in turn delays the next phase of the CSRD rollout.

For industries such as logistics, manufacturing, and other Scope 3-intensive sectors, what looks like a breather is in fact a strategic window of opportunity. The regulatory engine has not shut off; it is merely idling, and companies that use this intermission to optimize their emissions data flows, supplier engagement, and governance will be best placed when the lights go back on.

And while the “Stop-the-Clock” directive offers temporary relief from looming deadlines, it’s not a cancellation. It’s an intermission. A chance to get your systems, data, and strategy in order before the curtain rises again.

Key takeaway: The pause under the Stop-the-Clock directive is a strategic window, not a suspend button. Transition exposure and emissions liability are not diminishing; they are compounding. If you invest now in robust emissions data systems, supplier alignment, and transition planning, you will generate the highest return on climate investment (ROCI) when the regulatory regime fully takes effect.

Setting the stage: How we got here

When the CSRD was adopted in late 2022, it promised to reshape corporate transparency across Europe. By expanding the scope of mandatory sustainability disclosures to roughly 50,000 companies (up from around 11,000 under the old NFRD), the EU signalled that sustainability reporting should be treated with the same rigour as financial reporting. The board, the auditors, and the finance team can no longer treat environmental and social data as an ESG side topic. It is part of the financial result chain.

The CSRD mandated that companies disclose according to the European Sustainability Reporting Standards (ESRS) developed by EFRAG, covering topics from climate change to workforce management, biodiversity, and business conduct. Importantly, it required reporting on the entire value chain, meaning upstream suppliers and downstream customers alike would feel the ripple effects.

Original CSRD Timeline

That was the plan — until political and economic pressures, coupled with feedback from businesses and member states, pushed the Commission to re-evaluate the rollout.

Enter the Omnibus package and “Stop-the-Clock” directive

In spring 2025, the European Commission introduced the Omnibus package, a set of legislative “quick fixes” intended to streamline and simplify CSRD and related regulations. One element, the now-famous “Stop-the-Clock” directive, formally paused certain reporting obligations.4,5

What Stop-the-Clock Does

- Delays CSRD application by two years for Waves 2 and 3 (i.e., large companies not yet reporting and listed SMEs).

- Postpones CSDDD (Corporate Sustainability Due Diligence Directive) transposition and application by roughly one year.

- Allows “quick fix” transitional relief for Wave 1 companies to omit certain complex ESRS disclosures (e.g., Scope 3 or biodiversity) until FY 2027.

- Intends to enhance competitiveness and reduce reporting fatigue during a time of economic strain.

Critics argue that the pause risks undermining the EU’s credibility on sustainable finance. Proponents insist it’s a pragmatic step to ensure quality over haste. In either case, one truth remains: CSRD isn’t going away.

Key takeaway: The Stop-the-Clock directive buys time, not exemption. Companies still in scope will face even sharper scrutiny once reporting resumes.

What the 2025 trilogues will grapple with

As the trilogue negotiations get underway this autumn, expect several contentious topics to dominate the discussion.

a. Scope & thresholds

The Commission’s proposal to raise the company-size threshold to 1,000 employees (from the current 250) could exempt up to 80% of companies originally captured under CSRD. The Parliament, however, is likely to resist such broad exclusions, arguing that it would create uneven playing fields and distort value-chain transparency.

b. Scope-3 & value chain boundaries

Even if smaller entities are exempt, large manufacturers and logistics providers will still need supplier data to meet their own Scope-3 reporting obligations. This means pressure on smaller suppliers won’t vanish — it’ll just be informal. Expect discussions on proportionate data requests and simplified value-chain reporting templates.

c. Data granularity & ESRS simplification

EFRAG’s sectoral standards have drawn criticism for being excessively detailed. Negotiators may push to reduce datapoints and better align with ISSB/IFRS standards3 to ease the reporting burden. Additionally, EFRAG is also coming with their technical revision of the ERSRs as a technical advisor and has indicated that it aims to cut the number of mandatory data points by 50% or more in the revised ESRS.

d. Assurance requirements

Currently, CSRD requires limited assurance. A move toward reasonable assurance (similar to a full audit) could be deferred or phased in, particularly given resource constraints in audit markets.

e. Enforcement, penalties, and legal liability

Trilogues will likely refine the liability regime, clarifying whether executives can be held personally accountable for sustainability misstatements. The Directive sets the overall EU framework, but each member state will decide how (and whether) to hold directors or senior executives personally accountable for mis-disclosures. The key question is whether national laws will mirror the financial reporting liability regime, such as false statement rules, or whether sustainability will remain on a lighter enforcement track.

f. Interplay with CSDDD, Taxonomy, and CBAM

Harmonization across these frameworks remains critical. Expect debate over whether CSRD disclosures can serve as compliance evidence for related instruments like the Carbon Border Adjustment Mechanism (CBAM) or EU Taxonomy.

Key takeaway: Whether thresholds rise or data demands soften, the fundamental direction of travel, toward transparent and auditable sustainability data, isn’t reversing.

What the outcomes could mean for Scope-3 intensive industries

Regardless of where the trilogue lands, companies in logistics, manufacturing, and other Scope-3-intensive sectors should expect no free pass. Let’s consider three plausible scenarios:

Scenario A: High-ambition compromise

Thresholds rise slightly, some data points are simplified, but most large and multinational companies remain covered.

- Implication: Companies must continue building robust Scope-3 data systems and supplier engagement mechanisms.

- Risk: Compliance complexity remains high; smaller suppliers face indirect pressure to disclose.

Scenario B: Substantial rollback

Major carve-outs exempt mid-sized firms; reporting becomes lighter, limited assurance retained.

- Implication: Some relief for mid-tier players, but large firms still must gather data from exempt suppliers — shifting the burden rather than eliminating it.

- Risk: Data quality inconsistency; reputational risk for slow movers.

Scenario C: Full regime with extended timeline

No major rollback, but deadlines extended and implementation phased. This is the most unlikely scenario.

- Implication: Clear long-term visibility allows better system-building.

- Risk: Complacency could creep in; companies that delay preparation will face future bottlenecks.

Key takeaway: In every scenario, the carbon accounting capabilities you build now will be needed later — and likely rewarded by markets and regulators alike.

The “Stop-the-Clock” pause: What it means and how to use it

How companies have reacted so far

Some have breathed a sigh of relief while others have misread it as a signal to hit pause. The wiser companies — especially those in high-emission, complex supply chains — are using this time to stress-test their data pipelines, pilot supplier engagement tools, and refine governance structures.

What companies should be doing now

- Audit your data readinessMap where your sustainability data currently lives. This could be ERP, logistics systems or LCA tools. It could also be spreadsheets. Then assess data completeness for ESRS topics.

- Deepen supplier collaboration

Instead of waiting for mandatory requests, co-develop emissions calculation workflows with suppliers. This builds trust and saves time when the clock restarts. - Pilot internal reporting cycles

Treat FY 2025 and FY 2026 as “dry runs.” Practice data collection, validation, and reporting to spot inefficiencies early. - Align sustainability with finance

Integrate ESG and financial reporting systems. The CFO’s office must own as much of this process as the sustainability team.

- Quantify Return on Climate Investment (ROCI)

Treat decarbonization measures as portfolio investments. The faster you cut Scope 3 inefficiencies, the stronger your resilience to future carbon costs and market shifts.

Key takeaway: Use this regulatory intermission as your systems-building era. The companies that sprint during the pause will be the ones jogging comfortably when the race restarts.

Spotlight: A machine tool manufacturer’s “Pause Advantage”

Consider a leading European precision machine tools manufacturer — let’s call it EuroTech Tools AG. With over 10,000 employees and suppliers across Asia, Eastern Europe, and the Americas, EuroTech epitomizes a Scope-3-heavy operation.

When the Stop-the-Clock directive was announced, EuroTech’s sustainability steering group faced a choice: slow down to save cost, or double down to get ahead. They chose the latter.

Here’s how…

- Supplier segmentation: They divided their 3,000+ suppliers into high-, medium-, and low-impact categories, focusing initial efforts on the top 20 % of suppliers responsible for 80 % of emissions.

- Data digitalization: They implemented a central carbon data platform (like Cozero’s) to collect emissions data at product-line level, linking it directly to procurement and production systems.

- Carbon literacy training: Procurement staff were trained to interpret supplier data, enabling emissions to factor into purchasing decisions.

- Scenario simulation: They ran simulations on how future CSRD versions — high-ambition, rollback, or delay — would impact their disclosure workload and audit needs.

- ROCI tracking: Investments in data and supplier engagement were measured by cost savings from energy efficiency and material optimization.

Within 12 months, EuroTech had not only halved its emissions data gaps but also uncovered €4 million in annual cost savings through better resource management.

Key takeaway: The smartest companies treat regulatory pauses as pre-competitive accelerators, turning compliance work into operational efficiency gains.

The bigger picture: Carbon risk is financial risk

For logistics providers and manufacturers, carbon exposure is becoming a balance-sheet issue, not just a compliance metric.

- Carbon pricing mechanisms like the EU ETS and CBAM will increase operating costs for emissions-intensive imports and logistics routes.

- It is also critical to recognise the difference between carbon-accounting (which is about what your company emits) and climate-risk (which is about what climate change does to your business). Under CSRD both dimensions feature, but our focus is often skewed to Scope 3 emissions. For example: if your factory is in a flood-prone region, the physical risk from climate change is a climate-risk issue; meanwhile, the emissions your value-chain generates feed into your carbon-accounting. Banks and lenders increasingly evaluate both — and they expect credible transition and resilience plans.

- Investors are using sustainability disclosures as proxies for management quality and long-term viability.

The companies that act now to build data-driven emissions transparency will not only ensure compliance but also secure preferential financing, stronger customer retention, and strategic resilience in global value chains.

Key takeaway: Carbon literacy is the new financial literacy. Those who master both will outperform those who treat them as separate disciplines.

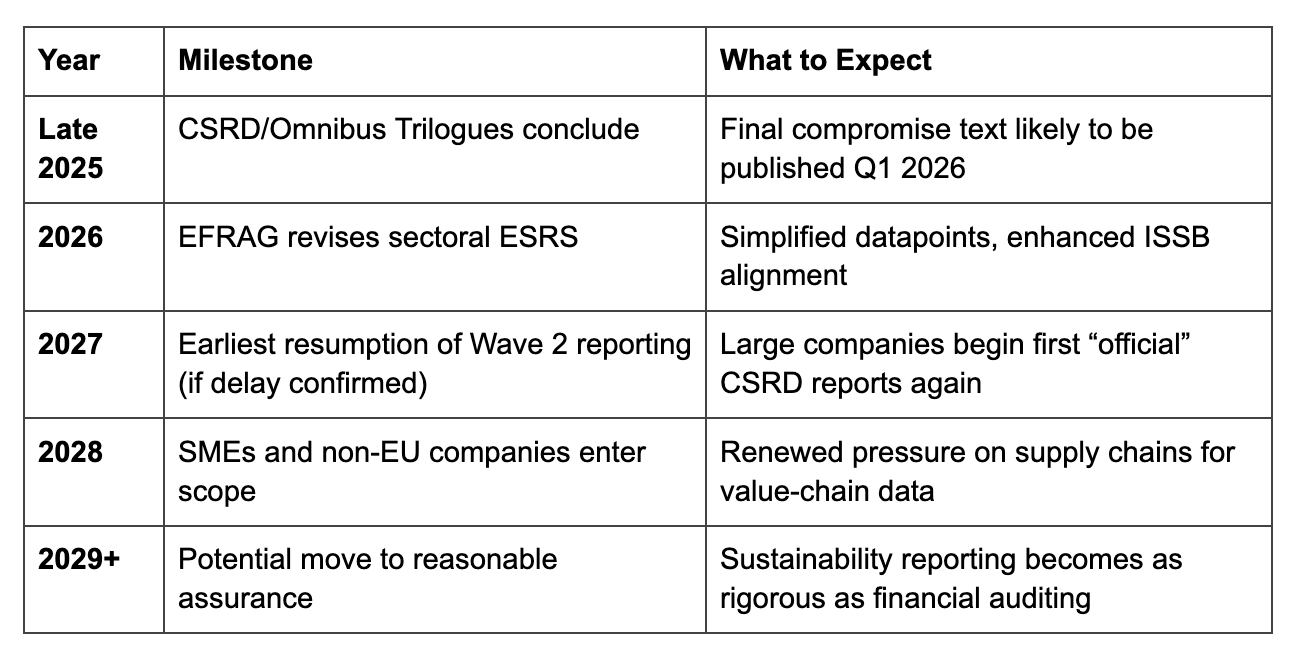

A forward-looking timeline: What happens next

The regulatory pendulum may swing, but the direction of travel is set: toward comprehensive, comparable, assured sustainability data that connects seamlessly with financial reporting.

What this means for logistics and manufacturing

Let’s ground this in sector specifics.

Logistics

- Fleet emissions and fuel data will face closer scrutiny, particularly under ESRS E1 (Climate Change).

- Modal shift data (road vs. rail vs. maritime) will likely be required in future sectoral standards.

- Client demand for verifiable transport emissions data will intensify, even if not yet legally mandated.

Manufacturing

- Product-level footprinting is becoming the norm, not the exception.

- Supplier engagement and lifecycle assessment (LCA) capabilities will directly impact future profitability.

- Automation of emissions data such as integrating MES, ERP, and sustainability platforms, will separate leaders from laggards.

Both sectors will also need to future-proof their operations against rising carbon prices, increasingly stringent customer procurement criteria, and potential public disclosure comparisons.

Key takeaway: Logistics and manufacturing firms that embed carbon data into daily decision-making will transform regulation into competitive advantage.

Strategy for the pause: Cozero’s readiness roadmap

At Cozero, we often say: “Carbon management is a team sport — but someone still has to keep score.” The Stop-the-Clock moment is your training camp. Here’s our recommended game plan:

1. Build the foundation

Set up a central data platform to capture emissions from all sources (Scope 1-3). Automate where possible, because manual reporting won’t scale.

2. Strengthen value-chain intelligence

Map supplier emissions, prioritize hotspots, and start pilot engagement programs.

3. Align governance & assurance

Integrate sustainability oversight into finance and audit committees. Prepare for future reasonable assurance requirements.

4. Simulate scenarios

Use scenario tools to test how each potential trilogue outcome would affect your workload, data needs, and cost exposure.

5. Quantify ROCI

Treat each decarbonization investment as a financial asset with measurable returns — from efficiency savings to reduced risk capital charges.

Closing thoughts: Don’t waste the intermission

The Stop-the-Clock directive gives industry two extra years on the CSRD calendar, but the planet’s carbon clock hasn’t stopped ticking. Nor has investor, customer, or lender expectation.

Whether you’re a logistics network managing intermodal freight or a precision manufacturer running energy-intensive machining centers, your future success depends on mastering emissions intelligence.

Final takeaway: The companies that drive ahead now by refining data, empowering suppliers, and integrating sustainability into finance, will own the narrative when reporting resumes.

Turn the Pause into Progress

At Cozero, we help Scope-3-intensive industries turn compliance readiness into climate performance. Our platform integrates carbon accounting, supplier collaboration, and financial insight — giving you the visibility to prepare confidently for whatever the trilogue outcome brings.

Don’t wait for the clock to restart. Turn your pause into progress.

Contact Cozero today to accelerate your Return on Climate Investment (ROCI) and build a sustainability reporting system that’s ready for whatever version of CSRD emerges next.

Endnotes

- European Parliament, MEPs to vote on simplified sustainability and due diligence rules in November, October 2025.

- European Commission, Omnibus Proposal for CSRD Simplification, COM (2025) 210 final, May 2025.

- Hogan Lovells, EU Omnibus Update – Recent Developments relating to CSRD and CSDDD – “quick fix” and more, May 2025.

- KPMG, EU releases Omnibus proposals, October 2025.

- Council of the EU, Press Release: Simplification: Council gives final green light on the ‘Stop-the-clock’ mechanism to boost EU competitiveness and provide legal certainty to businesses, April 2025.

- Grant Thornton, Omnibus package stop-the-clock proposal adopted by European Parliament, April 2025.

- Umweltbundesamt, European Sustainability Reporting Standards (ESRS) Berichtstandards, 2024.

- White & Case, EU Omnibus Package – Ten Things You Should Know About the Proposed Changes, March 2025.

- IEEFA, EU Omnibus ‘stop-the-clock’ proposal: A call for compromise, April 2025.

- ESGToday, EFRAG Aims to Cut Datapoints in European Sustainability Reporting Standards by at Least 50%, June 2025.

Related articles

Carrots and Sticks: How the EU ETS Review and Electrification Action Plan complement each other