The Carbon Border Adjustment Mechanism (CBAM) explained

As an essential part of the Fit for 55 package, CBAM creates incentives for non-EU producers to reduce emissions.

Get instant access

Link

What is the CBAM

The Carbon Border Adjustment Mechanism (CBAM) is an environmental policy instrument that aims to impose carbon costs on imported products equivalent to those faced by production facilities operating within the European Union (EU). CBAM is designed to prevent "carbon leakage" scenarios, where companies relocate their production to countries with laxer climate objectives.

Which goods are affected by CBAM?

CBAM focuses on imports of precursors, intermediate products, whose production is carbon intensive and at high risk of carbon leakage. Six sectors have been identified as relevant:

Finished goods, such as bikes or screwdrivers, are excluded from the regulation. CBAM Annex I specifies which input materials each sector should consider as precursors. The common nomenclature code (CN code) determines whether a good ultimately falls under the new regulation. You can find the list of CN codes in scope here under tab c_CodeLists.

Who is responsible for the reporting to CBAM?

The person who declares the importation of relevant goods inherits the CBAM reporting responsibility. This is typically the importer of goods but it can also be an indirect customs representative (e.g. when the importer is established outside of the European Union).

Customs will inform importers of CBAM goods of their reporting obligations at the moment of import.

What is the CBAM time frame?

1. Transitional Period

The regulation will be rolled out in a sequenced process, with the first transitional period starting on 01 Oct 2023 and lasting until the end of 2025. During this introductory period, the importer of affected goods shall submit a CBAM report on a quarterly basis (the first report covering Oct-Dec 2023 is due on 31 Jan 2024). No financial adjustments need to be paid for embedded emissions during this learning phase but significant fines may be imposed in case of non-compliance (e.g. not submitting a quarterly report).

2. Operational system

As of January 2026, a fully operational system is planned, in which reporting frequency changes to annually (declaration for the calendar year 2026 should be submitted by 31 May 2027). The report submission will be restricted to approved notifiers and reports will require external verification. Importers will also have to purchase a "CBAM commitment" in the form of allowances for every CBAM good imported into the EU at the average price of the EU Allowances*. The coverage of embedded emissions by the CBAM obligation will gradually increase from 2026 on as free allocation under the EU ETS is gradually phased out. Certificates can be purchased any time, and will be stored in the authorized declarant’s registered CBAM certificate account.

Operators of production facilities in third countries will be able to register in the CBAM registry and to make their verified embedded emissions from production of goods available to authorized CBAM declarants.

3. Developed system

As of January 2034, a fully developed system covering all embedded emissions will be effective (declaration for the calendar year 2034 to be submitted by 31 May 2035).

*EU Allowances (EUAs) are a type of carbon allowance that allows companies covered by the EU Emission Trading System (ETS) to emit a certain amount of CO2e. EUAs can be bought and sold on the market, and the variable market price of EUAs reflects the cost of reducing emissions.

What does CBAM reports should include?

- Quarterly breakdown of imported precursor quantity by CN codes, country of origin, production facility, and date of import (unlike in carbon accounting practices, the date of import is decisive, not the date of purchase).

- Embedded direct and indirect emissions of the precursor, including emissions from the production processes (heating, cooling, electricity) as well as those from materials consumed in the production process. For the first 3 quarters of the transitional period (until 31 July 2024), installations and importers could use default values for up to 20% of their emissions. However, starting from Q3 2024, actual emissions data from production facilities is required. This means tracking activities like fuel consumption and greenhouse gas concentrations directly from suppliers and manufacturers.

- Information about any carbon price that has already been paid in the imported precursor’s country of origin.

How can Cozero support organizations importing affected goods?

Collecting emissions data from all your suppliers is complex, time-consuming, and prone to errors. Ensuring accurate calculations and full compliance requires significant effort.

At Cozero, we develop a streamlined supplier engagement module to help suppliers generate emissions data more easily. Based on specific activities and data points, the system automatically calculates key details, which are then passed along to the company for use in their CO2 accounting. This solution not only reduces friction for suppliers but also ensures better quality and consistency in emissions reporting.

- Save time on supplier data management

Automate the collection of primary data from your suppliers, eliminating manual processes and reducing the risk of errors. Invite them to calculate CBAM-relevant Product Carbon Footprint data and share custom emission factors. - Centralize and document data collection requests

Leverage a centralized supplier data request history to stay compliant when using average emission data. The platform keeps track of your requests so you can easily demonstrate attempts to collect primary data. - Automate CBAM-related emission calculations

Apply supplier-specific emissions factors and automatically calculate imported goods emissions data granularly. Differentiate between direct and indirect emissions. - Reduce CBAM certificate costs and optimize your supply chain

Use our built-in CBAM dashboard to monitor the evolution of your emissions and costs over time. Analyze supply chain hotspots to identify low-emissions suppliers for strategic cost optimization.

Please do not hesitate to reach out if you have imported goods falling under this new regulation and wish to get support for your CBAM reporting! For more information, we also recommend checking out the European Commission’s dedicated CBAM website where you can find firsthand information.

Related articles

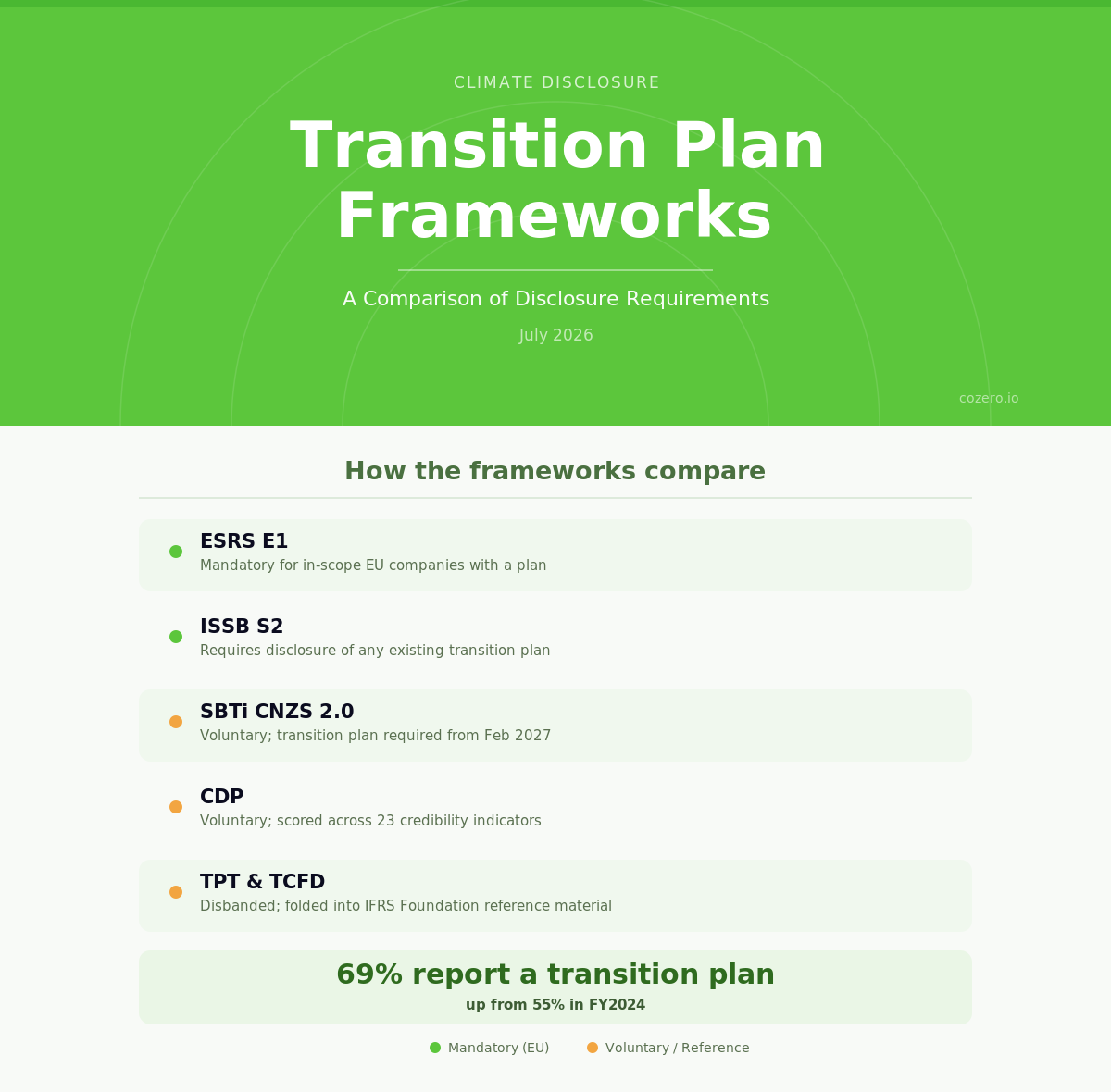

Climate Transition Planning Frameworks: A Comparison of Disclosure Requirements