Carbon Reporting Is Not Carbon Management

This article explores why sustainability and finance teams often work with disconnected data, and how companies can translate emissions into financial decisions, capital allocation, and real business value.

Get instant access

Link

Every year, sustainability teams spend months collecting emissions data. They build the report. They hit send. And then, mostly, nothing changes.

The data exists. The targets exist. But the plan to connect the two: one that finance teams can actually act on, usually does not. This article looks at why that gap exists, why it is becoming expensive, and what it actually takes to close it.

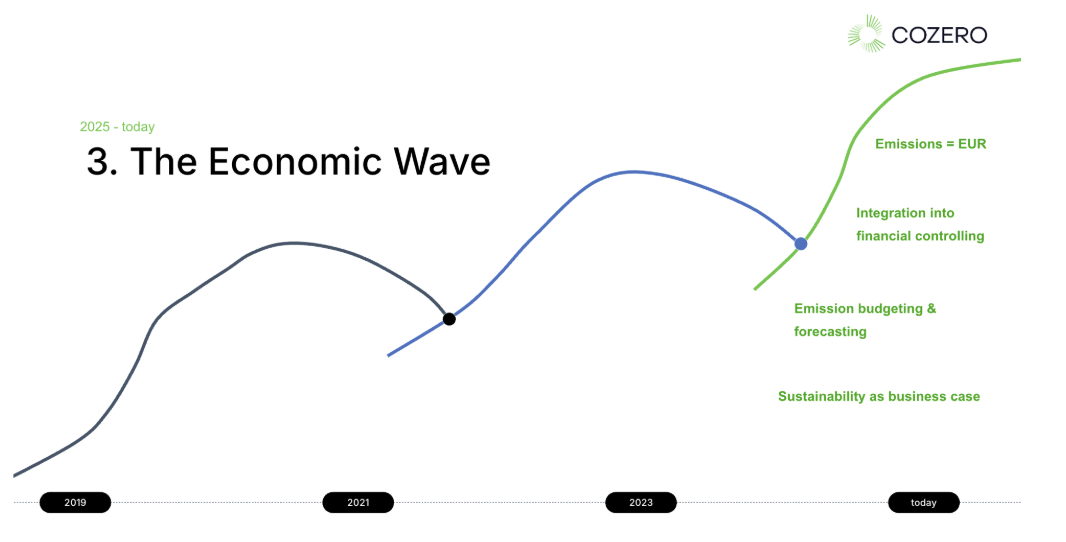

How We Got Here: Three Phases of Carbon Management

Corporate approaches to emissions have shifted significantly since 2019, and each phase left a different legacy.

Phase 1: Reputation (~2019–2022)

Companies rushed to claim "carbon neutral" status, mostly through offsetting. It was fast, it looked good, and it was largely inaccurate. Regulators and investors started asking harder questions. The era of easy claims ended.

Phase 2: Compliance (~2022–2024)

CSRD arrived. Scope 3 became unavoidable. Sustainability teams built reporting infrastructure. Companies learned to measure, document, and disclose. That was real progress, but it came with a hidden problem: most organisations built the machinery to report without building the machinery to act.

Phase 3: Economics (2025–today)

This is where we are now. Emissions are no longer just a reporting variable. They are a financial one. Carbon has a price through EU ETS, through CBAM, through green financing, through customer tenders. Companies that understand this are integrating decarbonisation into financial planning. The ones that do not are carrying a liability they have not yet put on the balance sheet.

Why This Year Is Different

Three things happened at once, and most finance and sustainability teams are still catching up.

CBAM went live on 1 January 2026. The Carbon Border Adjustment Mechanism has entered its definitive phase. If your company imports carbon-intensive goods into the EU - electricity, iron, steel, aluminium, cement, fertilisers, or hydrogen - you are now accumulating financial liability with every shipment. No certificates need to be purchased yet, but the clock is running. The first annual CBAM declaration and certificate surrender is due by 30 September 2027, covering all 2026 imports. Companies that are not tracking verified supplier emissions data today will be paying the maximum default rate in 2027.

CSRD Wave 1 reports landed in 2025. Around 11,000 large public-interest entities published their first CSRD-compliant sustainability reports this year. For every company in their supply chain, this is no longer a distant obligation. It is an incoming data request. If your customers are CSRD reporters, they will ask for your emissions data. If you cannot provide it, you become a liability in their supply chain.

The Omnibus package narrowed scope but not pressure. In 2025, the EU postponed CSRD Wave 2 and Wave 3 deadlines by two years, and removed roughly 80% of companies from scope entirely. Some companies took this as a signal to slow down. That is the wrong read. Wave 1 companies are still reporting. CBAM is still live. Investor and customer scrutiny has not paused. The companies using this window to build proper systems will be significantly ahead when the next deadlines hit.

The Real Gap: Sustainability Teams and Finance Teams Are Not Working From the Same Numbers

Here is a situation that plays out in a lot of companies right now.

A sustainability manager walks into a CFO meeting with a slide showing tonnes of CO₂ by scope and a reduction target for 2030. The CFO asks: "What does this cost us? What does it save us? When do we see a return?"

There are no answers ready. The meeting ends without a decision.

This is not a communication problem. It is a tooling problem. Sustainability teams are often working with frameworks like GHG Protocol and SBTi, which are designed for accounting and target-setting, not financial planning. They produce accurate numbers, but not the kind that drive capital allocation decisions.

According to CDP's November 2025 report "From Plans to Capital, Unlocking Credible Transition Finance at Scale", 72% of companies report emissions reduction initiatives. Only 11% disclose having any transition-aligned capital expenditures. Most companies are announcing intentions without committing resources. The data points to a clear opportunity. 51% of companies with transition plans identified growth and cost saving opportunities, nearly double the rate of companies without one. Yet only a small share translates these insights into capital allocation decisions. Companies that go one step further by linking transition plans to actual CapEx are the ones positioned to convert identified opportunities into realised returns. The financial work pays off. Most companies just are not doing it.

What "Acting on Carbon" Actually Looks Like

Moving from reporting to action means translating emissions data into financial language. That sounds abstract, so here is what it looks like in practice.

Putting a price on carbon internally. A shadow carbon price applied to your emissions changes your view of profitability. It reflects the carbon costs your business is increasingly exposed to, including compliance schemes, carbon taxes, supplier pass through, customer pricing pressure, and the rising cost of capital for high emission businesses. Without this, your EBITDA is an incomplete picture.

Building a decarbonisation CapEx plan. Not a roadmap with arrows and milestones. An actual multi-year capital plan that shows what investments are needed, when, and at what cost, in the same format your finance team uses for every other major expenditure. This is what makes the CFO conversation possible.

Evaluating investments with the full picture. A gas furnace versus an electric furnace looks different when you apply a carbon price to the emissions over time. Standard ROI misses this. A framework like ROCI (Return on Climate Investment) captures the full return: operational savings, avoided carbon costs, and revenue implications. The upfront cost is only part of the story.

Sequencing reductions by cost and impact. Not all reduction measures are equal. Marginal Abatement Cost Curve (MACC) analysis lets you prioritise initiatives rationally, highest impact at lowest cost first, rather than reacting to whoever made the loudest case in the last meeting.

None of this requires starting from scratch. It requires connecting the sustainability data you already have to the financial frameworks your organisation already uses.

The Window to Act Wisely Is Now

CBAM certificate costs are accumulating in 2026, payable in 2027. CSRD supply chain data requests are already arriving. Carbon pricing is structural, not temporary.

The companies building financially grounded decarbonisation plans today are not just reducing compliance risk. They are finding cost savings and competitive positions that their competitors are missing.

The gap between knowing your emissions number and knowing what to do with it is closeable. It just requires treating carbon as what it actually is: a financial variable, not a reporting obligation.

Sources:

CDP, "From Plans to Capital: Unlocking Credible Transition Finance at Scale", November 2025. https://www.cdp.net/en/insights/from-plans-to-capital Last accessed April 1, 2026

European Commission, CBAM definitive phase entry into force, January 2026. https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en Last accessed April 1, 2026

Related articles

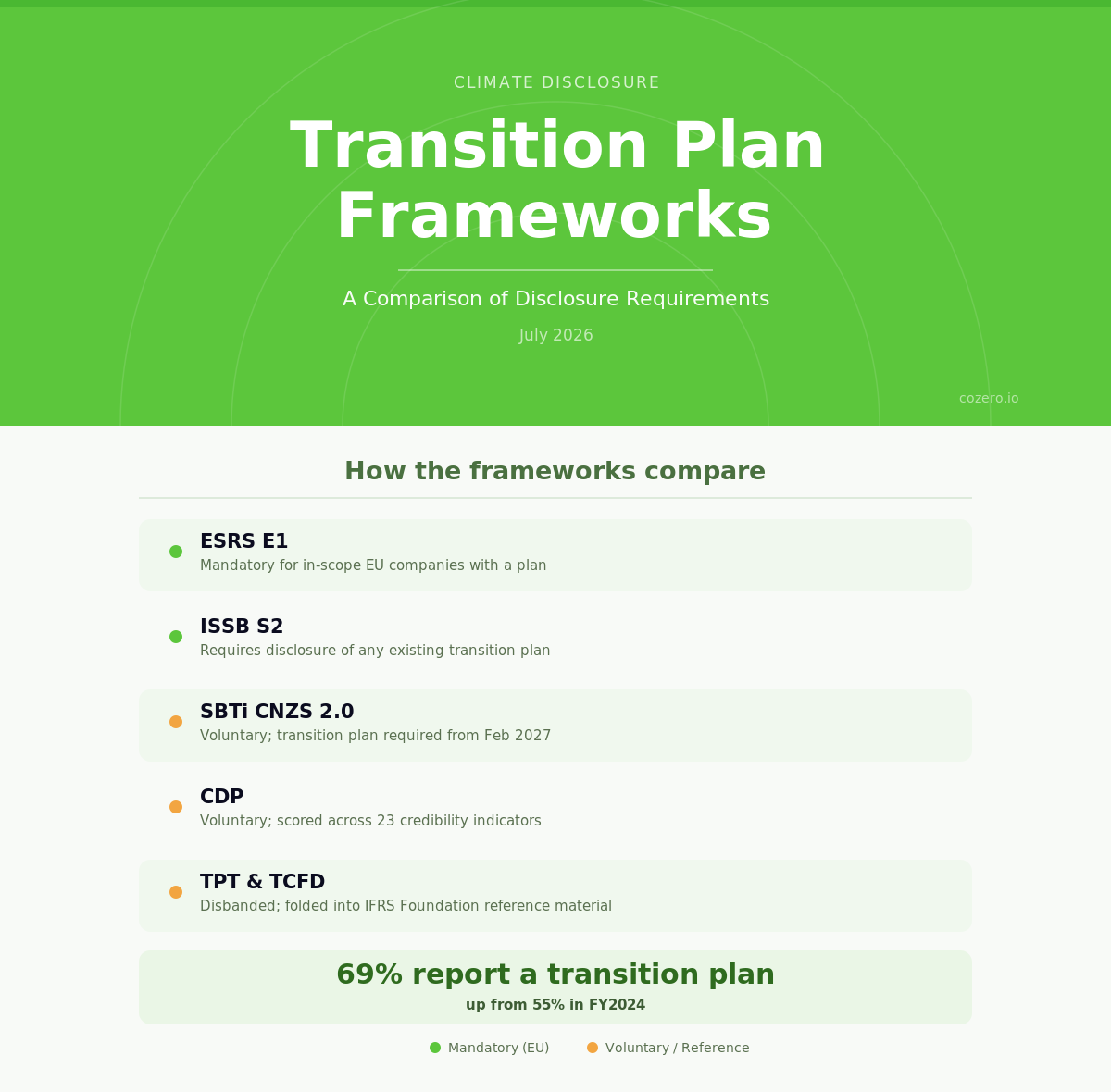

Climate Transition Planning Frameworks: A Comparison of Disclosure Requirements