Die Corporate Sustainability Reporting Directive (CSRD) erklärt

Immer mehr Umweltvorschriften, die direkt oder indirekt mit der CO2-Bilanzierung zusammenhängen, wirken sich auf Unternehmen aus, die in der Europäischen Union tätig sind. Dazu gehört die Richtlinie Corporate Sustainability Reporting Directive (CSRD).

Get instant access

Link

Ein Eckpfeiler in der der europäischen grünen Transformation

In den letzten Jahren hat die Europäische Union intensiv an der Corporate Sustainability Reporting Directive (CSRD) gearbeitet, einer wichtigen gesetzgeberischen Maßnahme des EU Green Deals. Die CSRD ist ein "entscheidender Schritt zur Zielsetzung, Nachhaltigkeitsberichterstattung auf Augenhöhe mit der Finanzberichterstattung zu platzieren. Qualitativ hochwertige nachhaltigkeitsbezogene Informationen sind in der Tat entscheidend für Transparenz und Entscheidungsfindung." (Patrick de Cambourg, Vorsitzender des EFRAG SRB)

Am 31. Juli 2023 hat die Kommission die European Sustainability Reporting Standards (ESRS), ein Bündel an zwölf Offenlegungsstandards, verabschiedet. Diese allgemeinen und nachhaltigkeitsbezogenen Standards wurden in Zusammenarbeit mit bestehenden Rahmenwerken wie dem Global Reporting Initiative (GRI), dem Carbon Disclosure Project (CDP) und der Task Force for Climate-related Disclosures (TCFD) entwickelt, um die Harmonisierung und Vergleichbarkeit von Nachhaltigkeitsberichten sicherzustellen. Es wird geschätzt, dass die CSRD mehr als 50.000 Unternehmen betrifft, die in der EU ansässig sind oder auf EU-Territorium tätig sind.

Der folgende Artikel erläutert den Anwendungsbereich, den Zeitplan und die wichtigsten Merkmale des ESRS. Er hebt hervor, wie Cozero Unternehmen dabei unterstützen kann, sich effizient an die CSRD anzupassen. Bei Cozero sind wir der Meinung, dass die CSRD über die Einhaltung gesetzlicher Vorschriften hinaus als strategisches Erfordernis für Organisationen betrachtet werden muss, um im Hinblick auf eine kohlenstoffarme europäische Wirtschaft wettbewerbsfähig zu bleiben.

Welche Unternehmen sind betroffen und wann müssen Berichte eingereicht werden?

- Große öffentlichkeitswirksame EU-Unternehmen, die der EU-Richtlinie zur nichtfinanziellen Berichterstattung (NFRD) unterliegen, dem bislang geltenden Offenlegungsgesetz für öffentlichkeitswirksame Unternehmen > 500 Mitarbeiter*innen

- Andere große EU-Unternehmen, die zwei der drei Bedingungen erfüllen, werden zur Berichterstattung gemäß der CSRD verpflichtet sein, auch wenn sie zuvor nicht der NFRD unterlagen

- 50 Millionen Euro Nettoumsatz

- 25 Millionen Euro Vermögen

- 250 oder mehr Mitarbeiter

- Nicht-EU-Unternehmen, die in zwei aufeinanderfolgenden Jahren einen Gesamtumsatz von über 150 Millionen Euro erzielt haben, mit einem jährlichen Nettoumsatz einer EU-Niederlassung von 40 Millionen Euro

- Gelistete europäische KMUs müssen Berichte unter Verwendung vereinfachter Standards erstellen

- Vorschlag der Kommission: separate freiwillige Standards für nicht gelistete KMUs

Wie sind die ESRS aufgebaut und was sind die Hauptmerkmale?

Doppelte Wesentlichkeit: Es gibt zwei Wesentlichkeitsdimensionen, die bewertet werden müssen, nämlich financial und impact. Ein Nachhaltigkeitsaspekt ist aus financial Sicht wesentlich, wenn er potenziell erhebliche finanzielle Auswirkungen auf das Unternehmen auslösen und zukünftige Cashflows und Unternehmenswert beeinflussen kann. Ein Nachhaltigkeitsaspekt ist aus Impact-Sicht wesentlich, wenn er mit erheblichen Auswirkungen des Unternehmens auf Menschen oder die Umwelt verbunden ist.

.png)

Unternehmen werden diejenigen Standards offenlegen müssen, die aus einer oder beiden Dimensionen wesentlich sind. Die doppelte Wesentlichkeit ist das Herzstück der CSRD und definiert den Umfang der Informationen und Bereiche, die offengelegt werden müssen. Unternehmen müssen eine klare Governance-Struktur definieren, um wesentliche Themen strategisch anzugehen, sowie relevante physische und monetäre KPI-Daten sammeln.

Aufbau der Standards:

Umfassende und integrierte Berichterstattung: Ein Hauptaugenmerk künftiger Compliance liegt auf der Verfügbarkeit und Robustheit von Nachhaltigkeitsdaten. Als integraler Bestandteil des Managementberichts wird die Nachhaltigkeitsberichterstattung auf Augenhöhe mit der finanziellen Berichterstattung veröffentlicht. Darüber hinaus unterliegen Unternehmen einer Überprüfung ihrer Daten, die klare Prüfpfade sowie Prozessdokumentation und -kontrollen erfordert. Nichteinhaltung kann zu Sanktionen führen.

Wie Cozero Unternehmen bei der Einhaltung des CSRD-Klimastandards unterstützt

1. Arbeiten Sie zusammen, um umfassende Fähigkeiten in den Bereichen CO2-Bilanzierung und strategische Dekarbonisierung aufzubauen

Die Nachhaltigkeitsberichterstattung wird mit der CSRD von hoher Relevanz und Komplexität sein. Für Unternehmen bedeutet dies, umfassende und breite Nachhaltigkeitsfähigkeiten in gleich mehreren Bereichen aufzubauen, einschließlich des CO2-Accountings. Darüber hinaus müssen zahlreiche interne Abteilungen einbezogen werden und ausreichende Ressourcen zur Verfügung stehen.

Cozeros Lösungen ermöglichen es Organisationen, gemeinsam an einem tiefen Verständnis von a) Unternehmens- und Product Carbon Footprints und b) Maßnahmen zur CO2-Reduktion zu arbeiten und eine maßgeschneiderte Dekarbonisierungsstrategie zu entwickeln.

2. Eine einfache Möglichkeit, eine qualitativ hochwertige Berichterstattung über den Klimawandel sicherzustellen

Das CSRD legt großen Wert auf Datengenauigkeit und Qualität. Eine unabhängige Qualitätssicherung wird nicht nur die Richtigkeit der angegebenen Endpunkte überprüfen, sondern auch die Plausibilität und Robustheit der Datenerhebungs- und Berechnungsmethoden berücksichtigen. Darüber hinaus verlangt die Verordnung wahrscheinlich, dass Unternehmen ein maschinenlesbares Kennzeichnungssystem für die Meldung von Informationen verwenden. Daher muss der Bericht im XTHML-Format erstellt und die Informationen digital gekennzeichnet werden, damit sie in der kommenden ESAP-Datenbank (European Single Access Point) verfügbar sind.

Bei Cozero möchten wir sicherstellen, dass Sie eine genaue CO2-Bilanzierung und eine kohärente Dekarbonisierungsstrategie entwickeln. Wir unterstützen unsere Kunden während des gesamten Prozesses der Erfassung und Eingabe relevanter Daten zum CO2-Fußabdruck von Unternehmen und Produkten und führen eine Qualitätssicherung der Berechnungen durch, um Datenmängel zu erkennen. Unsere Emissionsfaktoren und -methoden basieren zwar auf dem neuesten Stand der Forschung, doch die Berechnungen werden automatisch ausgeführt, wodurch Genauigkeit garantiert wird. Schließlich wollen wir an Verknüpfungen zwischen unserer Plattform und dem digitalen Tagging-System arbeiten, damit unsere Kunden Informationen problemlos untereinander verbreiten können.

Related articles

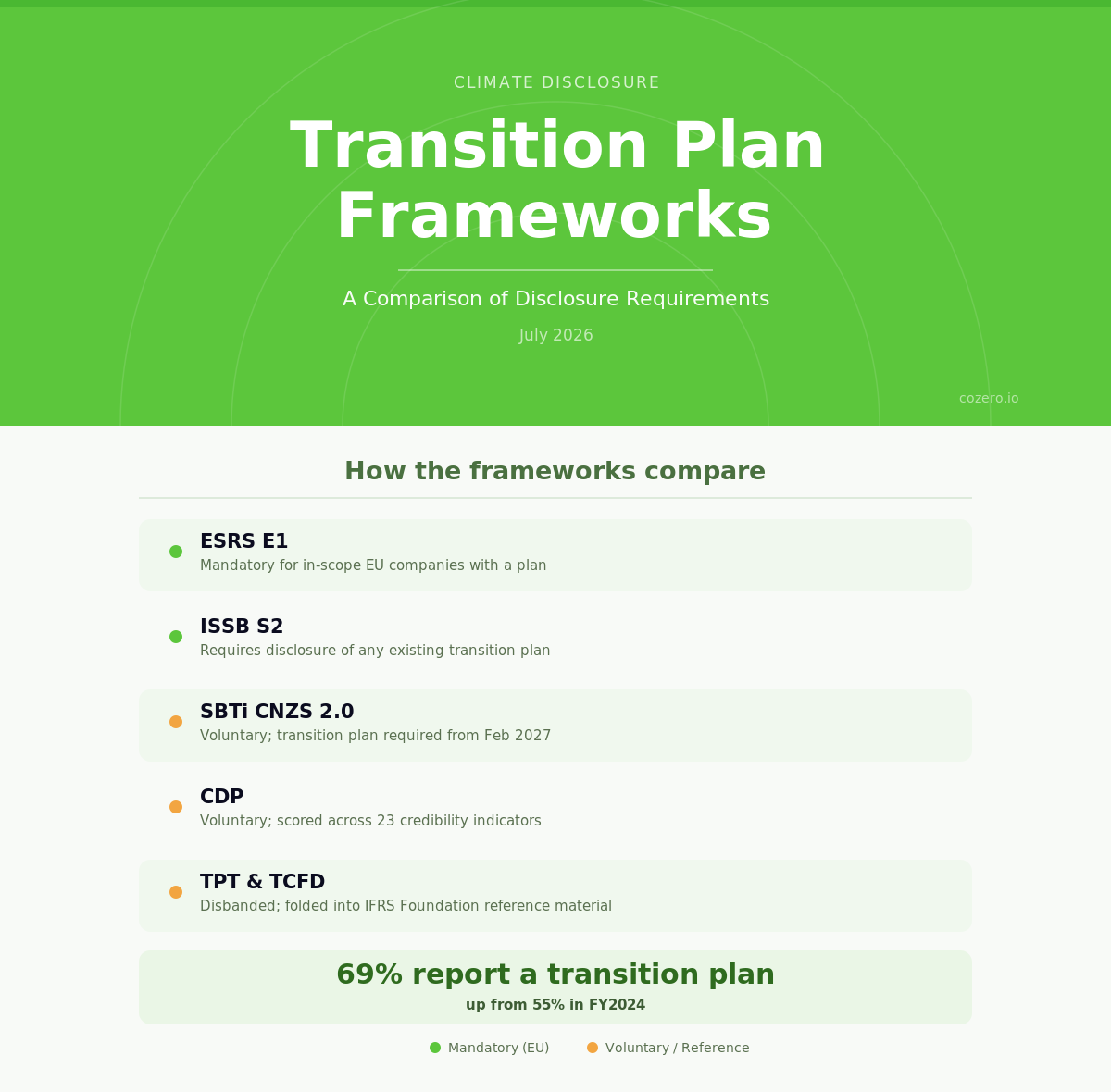

Climate Transition Planning Frameworks: A Comparison of Disclosure Requirements